{kind=link}

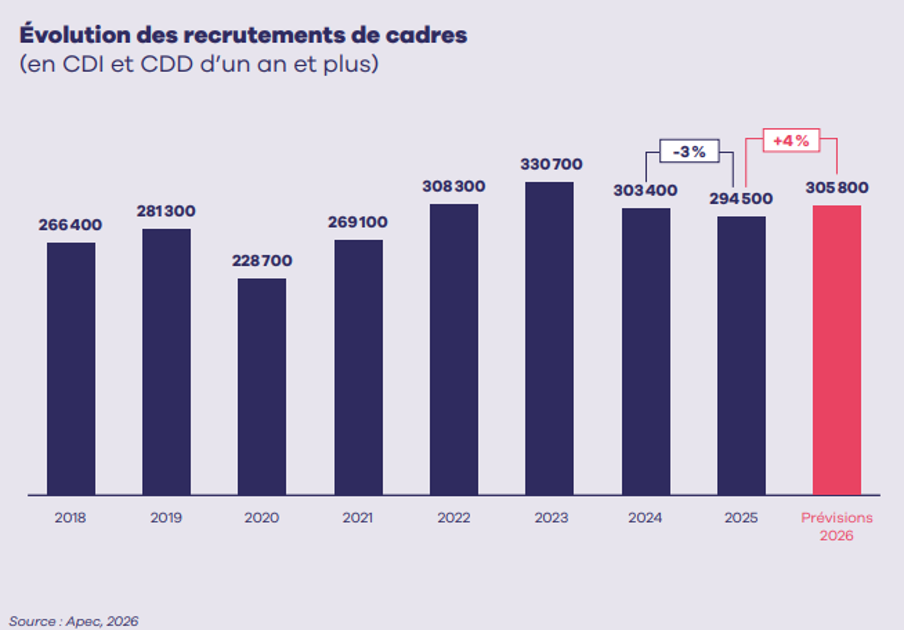

The market is picking up again. That’s the key point. But the landscape is very different from that of 2023. The upturn in 2026 doesn’t rekindle the euphoria of the boom years, nor the mass hiring driven solely by “digital transformation.” The trend outlined by Apec looks more like a restart under constraints: more recruitment, yes, but for more targeted positions, in more clearly defined talent pools, and with significantly higher expectations for operational impact. IT remains the primary driver of the executive job market, with 61,160 recruitments anticipated in 2026, in a global market projected at 305,800 hires. In other words, demand is returning, but with stricter criteria.

The Apec study is based on an annual survey of 8,100 private sector companies in metropolitan, representative by region, size, and sector. It measures the recruitment of managers on permanent and fixed-term contracts of one year or more , as well as internal promotions and departures. It therefore does not encompass the entire tech market in the broadest sense: neither all freelancing, nor short-term assignments, nor the full range of subcontracting outside of traditional managerial positions.

The 2026 rebound exists, but it remains modest and conditional.

2025 left a real lull, without tipping into collapse.

The 2026 recovery cannot be understood without considering the 2025 trough. Last year, French companies recruited 294,500 managers , a 3% year-on-year decrease. While this decline appears less dramatic than that of 2024, the cumulative drop compared to the 2023 peak reaches 11% .

The market has therefore lost momentum, but not its backbone. The machine hasn’t broken down; it has slowed down, sometimes sharply, due to deteriorating economic visibility and business investment that has remained almost at a standstill.

This slowdown primarily affected the segments that usually drive managerial employment. In 2025, engineering and R&D declined by 6% , IT activities by 4% , and consulting by 3% .

At the same time, household consumption increased by only 0.4% , business investment by 0.2% , and French growth by 0.9% .

2026 sees recruitment exceeding 300,000 again, without reaching the top spot.

The 2026 forecast should therefore be interpreted for what it is. Apec projects 305,800 executive-level hires , representing a 4% year-on-year increase. The symbolic threshold of 300,000 hires has moved back into positive territory. The market is regaining momentum. However, it has not yet returned to the level of 330,700 hires observed in 2023.

The same nuance applies to IT. Information technology remains the top recruitment area with 61,160 planned hires , ahead of research and development and sales. This volume confirms the continued centrality of tech jobs in the private sector.

But again, this isn’t a euphoric recovery . The market is picking up because certain needs can no longer be put on hold: modernization, cybersecurity, AI , infrastructure, project execution. Not because all companies are massively reopening the floodgates.

Why does this increase remain under surveillance?

Apec does not present 2026 as a certainty year, but as a turning point. Its projection remains tied to several highly sensitive variables: business investment, the cost of credit, the level of inflation, foreign trade, and the geopolitical situation in the Middle East.

The point of fragility is clear: if energy prices rise again and interest rates rise, investment will once again take a hit, with an immediate effect on the recruitment it fuels.

The section of the study dedicated to risks states it unequivocally: an energy crisis linked to the regional conflict would put pressure on prices, consumption, financing decisions, and, consequently, on business projects. This is why the 2026 rebound looks less like a secure new cycle than a restart under constant monitoring . An improvement, yes. A definitively consolidated foundation, no.

Where the recovery is really concentrated: sectors, regions, occupational groups

High value-added services are regaining control.

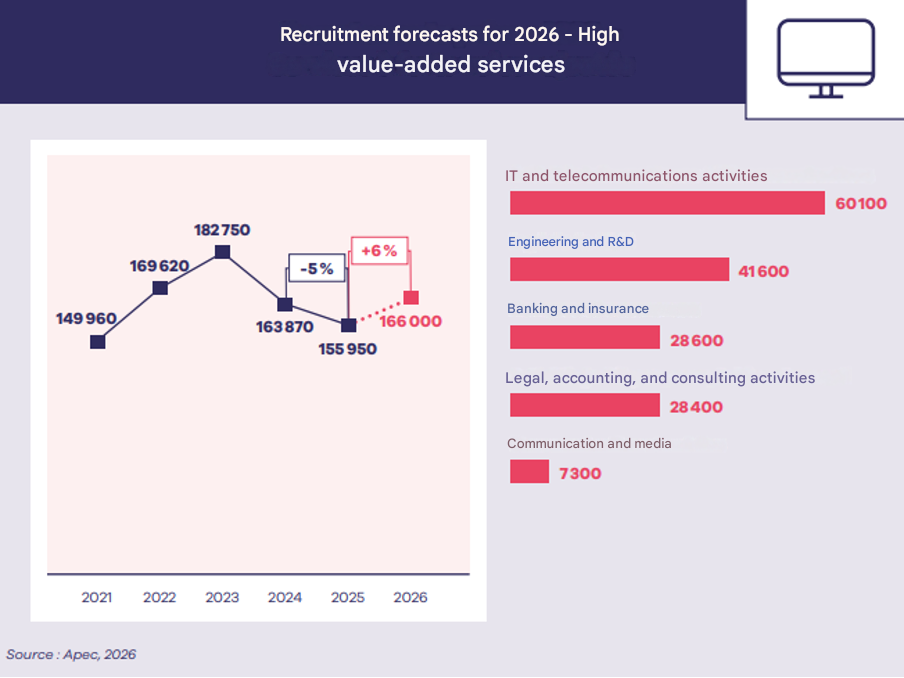

The recovery is not coming from everywhere, uniformly. It is concentrated first in high value-added services , with 166,000 executive recruitments anticipated in 2026, or +6% .

This is where IT regains its driving role, alongside engineering-R&D and consulting. In detail, IT activities grew by 5% , engineering -R&D by 7% , consulting by 6% and banking-insurance by 9% .

Conversely, media communication remains in retreat, and other services show a much more contrasting picture, between stabilization, decline or limited progress.

This sector-based approach reveals something very concrete. The market doesn’t indiscriminately reward all segments of the core economy. It reinvigorates areas where investment directly creates value , structures execution, or supports a competitive advantage. IT is no longer simply a cost center to be contained or a promise of innovation to be showcased in an annual report. It is once again becoming a lever for production, security , and acceleration.

The geography of the rebound paints a fairly clear map

The regional map shows a diffuse but not homogeneous restart.

The Île-de-Us region remains the critical mass of the executive market with 143,160 recruitments , representing 47% of the national total, and an expected increase of 5% .

Auvergne-Rhône-Alpes follows with 35,260 hires and +3% , driven by a mixed fabric, both industrial and tertiary with high technological intensity.

PACA-Corse sees a rise of 18,800 recruitments and +4% after two significantly more turbulent years.

Occitanie , finally, shows the most marked progress with 19,500 recruitments and +6% , against a backdrop of good performance in the aeronautics sector and a robust local ecosystem.

The stabilization areas tell a different story. The Grand Est and Bourgogne-Franche-Comté regions are stagnating. Normandy and Hauts-de- are barely recovering. The signal sent by this geography is not only economic; it also affects the productive structure.

Why recruitment is picking up again: investment, cybersecurity, AI, delivery

The real driver of the rebound remains the return of investment budgets

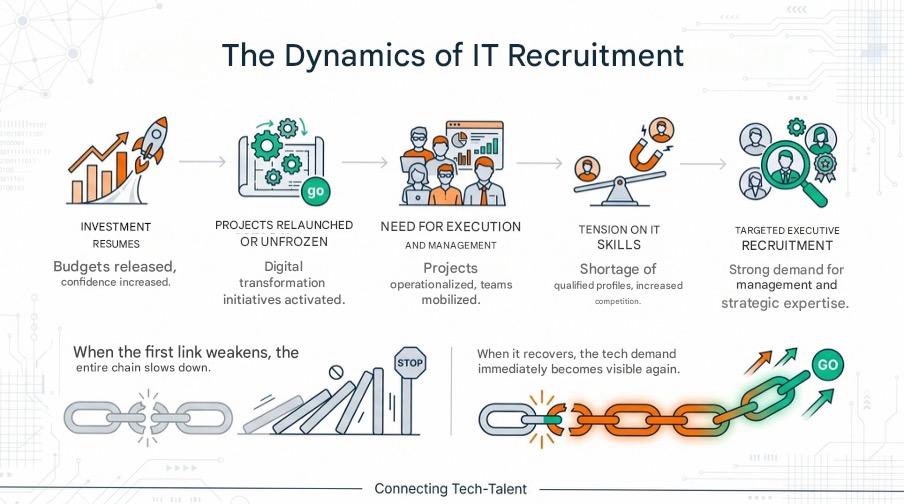

The framework market doesn’t recover on its own. It follows investment. The study clearly indicates this: the expected improvement by 2026 hinges on a 1.2% increase in business investment , after two years of decline or stagnation. This is the fundamental driver. When budgets pick up again, even modestly, frozen projects are put back on the agenda, roadmaps regain momentum, and recruitment opportunities most directly linked to execution resume.

In IT, the link is almost automatic. A return on investment isn’t just more money on the table. It’s a reassessment of priorities: modernizing an aging stack, consolidating a cloud platform that has become too fragmented, taking over costly technical debt, industrializing a data pipeline, raising a level of security that can no longer handle the load…

Executive recruitment then acts as a direct extension of the investment decision.

and AI are no longer confined to the laboratory.

Apec explicitly links IT demand to three drivers: digital transformation, strengthening of cybersecurity and the rise of artificial intelligence.

By 2026, cybersecurity and AI will no longer be considered merely “innovative topics.” They will shift into the category of operational capabilities. The question will no longer be about testing a topic, but about integrating it into a real-world information system, subject to constraints of security, governance, cost, maintenance, and compliance.

This is where the market for AI professionals is tightening again. An organization that industrializes AI applications isn’t just looking for someone capable of prototyping. It’s also looking for skills in architecture, data quality, security, MLOps , risk management, and integration with existing workflows. The same is true in cybersecurity: between resilience requirements, increased infrastructure exposure, a proliferation of attack surfaces, and stricter internal requirements, recruitment is less about theoretical awareness and more about the ability to maintain production without disrupting delivery.

Young professionals are benefiting less from the recovery

Recruitment of managers with less than six years of experience is only increasing by 1% in 2026, to 137,600 hires , which is still well below 2024 and, even more so, below the peak of 2023.

Conversely, candidates with 6 to 10 years of experience are seeing a 16% increase in recruitment intentions. The market preference is clear: when uncertainty remains high, companies favor those who can quickly become productive.

This bias doesn’t mean that career opportunities are closing everywhere. It says something else: in a year that is still unstable, recruitment becomes a trade-off between speed and risk.

Intermediate profiles are more reassuring because they require less time to get up to speed, more easily maintain a cross-functional relationship, and better withstand the pressure of delivery.

How can we prepare for this rebound without overinterpreting it?

Make the delivered value visible, not just the stack

The rebound primarily benefits those profiles that document a career path, not just a collection of tools. A strong CV or profile in 2026 gains weight when it links technical skills to concrete results. The skillset matters. The story it tells often carries more weight.

In fact, a clear path highlights four pieces of evidence:

- the arbitrations actually held;

- the absorbed friction;

- the measurable results obtained;

- the level of autonomy over a critical perimeter.

Signals to watch for in the second half of 2026

The restart will either be confirmed or will settle down around a few very observable indicators.

First, the actual level of investment by companies .

Then there is the depth of the offerings in cloud, cyber, data, infrastructure and delivery professions.

Finally, the actual space given to profiles with less than six years of experience remains the best thermometer of a broad recovery or, on the contrary, of a market that is still tense.

IT recruitment in 2026: an improvement?

The IT executive market is indeed picking up again in 2026. But this recovery doesn’t resemble a general slowdown. It looks more like a re-evaluation. Companies are reopening positions where IT directly supports execution, security, transformation, and growth. They are recruiting less based on intuition and more on proven track records.

This is undoubtedly the real turning point of the year. IT remains the driving force behind executive recruitment, but this driving force operates with tighter tolerances . Concrete impact, ability to deliver, risk management, clarity of role, exposure to the macroeconomic context: this is the new regime.